Conventional loans and USDA loans are two common types of home loans, but there are some key differences between them. Conventional loans are offered by private lenders, while USDA loans are backed by the U.S. Department of Agriculture.

Conventional loans typically have stricter credit and income requirements than USDA loans. USDA loans are available to borrowers with lower credit scores and incomes, and they can be used to purchase homes in rural areas.

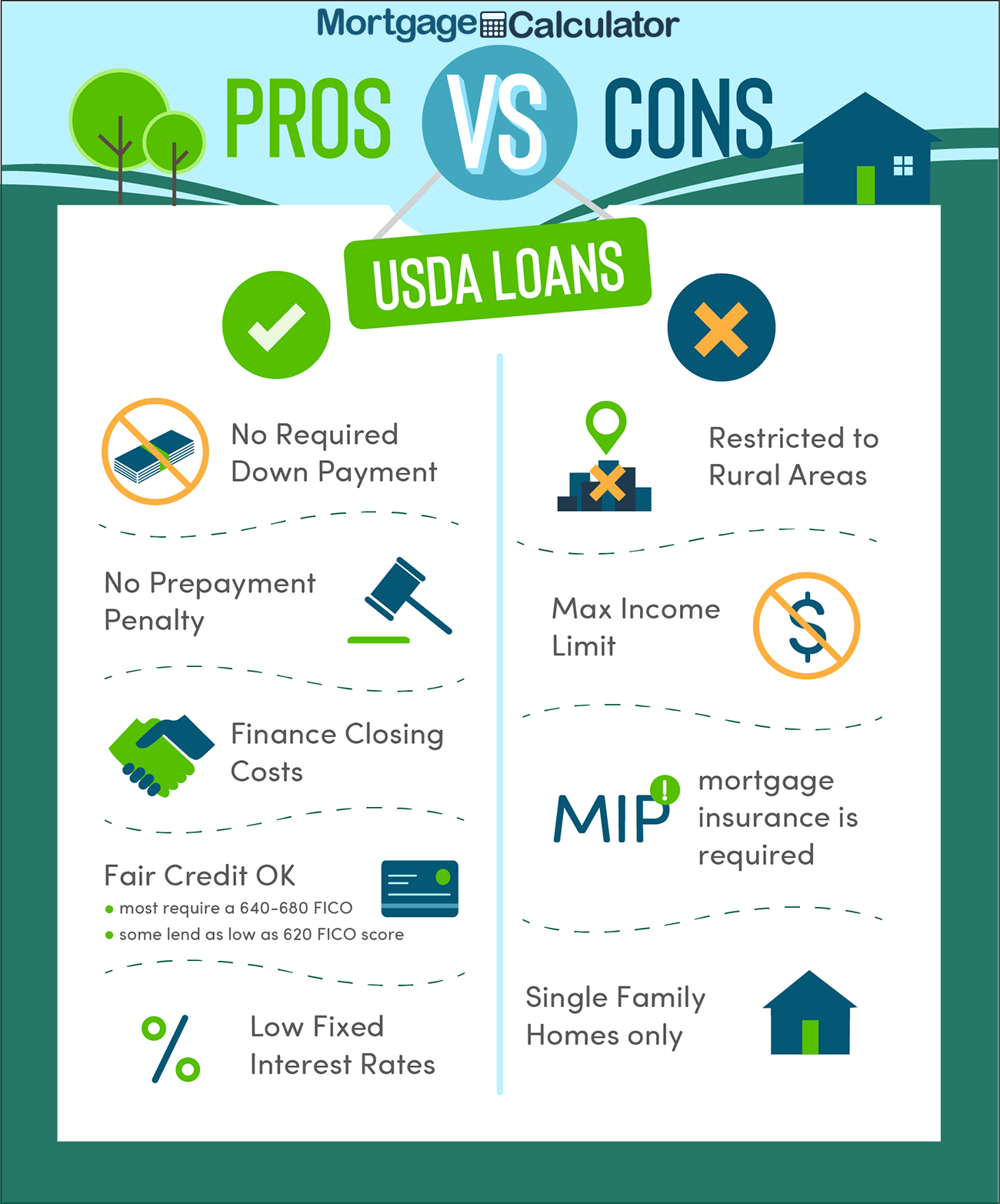

USDA loans also have lower interest rates than conventional loans, and they can be financed with no down payment. However, USDA loans have some restrictions that conventional loans do not. For example, USDA loans can only be used to purchase homes in eligible rural areas, and they have income limits for borrowers.

Ultimately, the best type of loan for you will depend on your individual circumstances. If you have a good credit score and income, a conventional loan may be a good option. If you have a lower credit score or income, a USDA loan may be a better choice.

Here is a table that summarizes the key differences between conventional loans and USDA loans:

Conventional vs USDA Loans

When considering a home loan, understanding the differences between conventional and USDA loans is crucial. Here are 8 key aspects to consider:

- Loan Type: Conventional loans are offered by private lenders, while USDA loans are backed by the US Department of Agriculture.

- Credit Requirements: Conventional loans typically have stricter credit requirements than USDA loans.

- Income Requirements: USDA loans have more flexible income requirements compared to conventional loans.

- Down Payment: Conventional loans often require a down payment, while USDA loans can be obtained with no down payment.

- Interest Rates: USDA loans generally offer lower interest rates than conventional loans.

- Loan Limits: Conventional loans have higher loan limits than USDA loans.

- Property Location: USDA loans are restricted to rural areas, while conventional loans can be used for properties in any location.

- Borrower Eligibility: USDA loans are available to low- to moderate-income borrowers, while conventional loans have no such restrictions.

These key aspects highlight the distinct features of conventional and USDA loans. Conventional loans provide more flexibility in terms of property location and borrower eligibility, but may have stricter credit and income requirements. USDA loans, on the other hand, offer more favorable terms for low- to moderate-income borrowers in rural areas, but come with restrictions on property location and loan limits.

1. Loan Type

The distinction between conventional loans and USDA loans is rooted in their respective sources of funding. Conventional loans are offered by private lending institutions, such as banks and mortgage companies. These lenders operate under standard lending guidelines and assess borrowers based on their creditworthiness, income, and debt-to-income ratio. USDA loans, on the other hand, are backed by the United States Department of Agriculture and are designed to promote homeownership in rural areas.

This fundamental difference in loan type has several implications. Firstly, conventional loans are subject to the lending standards set by individual lenders, which can vary depending on the institution's risk tolerance and target market. USDA loans, however, adhere to specific guidelines established by the USDA, ensuring a more consistent lending process and potentially more favorable terms for borrowers who meet the eligibility criteria.

The practical significance of understanding the loan type distinction lies in its impact on the loan application and approval process. When applying for a conventional loan, borrowers must go through the lender's underwriting process, which involves a thorough evaluation of their financial history and current financial situation. USDA loans, on the other hand, have a more streamlined application process, with less stringent credit and income requirements, making them more accessible to borrowers with lower credit scores or limited financial resources.

In summary, the loan type distinction between conventional loans and USDA loans is a crucial factor to consider when exploring home financing options. Conventional loans offer greater flexibility and may be suitable for borrowers with strong credit profiles, while USDA loans provide more favorable terms and accessibility for borrowers in rural areas or with lower credit scores.

2. Credit Requirements

The difference in credit requirements between conventional loans and USDA loans is a significant factor to consider when exploring home financing options. Conventional loans, offered by private lenders, generally have stricter credit requirements than USDA loans, which are backed by the US Department of Agriculture. This distinction stems from the varying risk assessments and lending criteria employed by private lenders and government-backed programs.

For conventional loans, lenders evaluate a borrower's credit history, including factors such as credit score, payment history, and outstanding debts. Borrowers with higher credit scores, typically above 620, are considered lower risk and may qualify for more favorable loan terms, including lower interest rates and higher loan amounts. USDA loans, on the other hand, have more flexible credit requirements, recognizing that borrowers in rural areas may have limited access to traditional credit products.

The practical significance of understanding the difference in credit requirements lies in its impact on loan eligibility and affordability. Borrowers with lower credit scores may find it challenging to qualify for conventional loans or may only be approved for smaller loan amounts at higher interest rates. USDA loans, with their more lenient credit requirements, provide an alternative path to homeownership for these borrowers, allowing them to overcome credit-related barriers.

In summary, the stricter credit requirements for conventional loans compared to USDA loans reflect the varying risk profiles and lending mandates of private lenders and government-backed programs. This distinction has a direct impact on loan eligibility, affordability, and access to homeownership for borrowers with different credit histories.

3. Income Requirements

When comparing conventional loans to USDA loans, the difference in income requirements is a crucial factor to consider. Conventional loans, offered by private lenders, typically have stricter income requirements than USDA loans, which are backed by the US Department of Agriculture. This distinction is rooted in the varying risk assessments and lending criteria employed by private lenders and government-backed programs.

- Debt-to-Income Ratio (DTI): Conventional loans often have stricter DTI requirements, limiting the amount of monthly debt payments relative to a borrower's income. USDA loans, on the other hand, may allow for higher DTIs, recognizing that borrowers in rural areas may have additional expenses or limited income sources.

- Income Sources: Conventional loans typically consider traditional sources of income, such as wages, salaries, and investments. USDA loans, however, have more flexibility in considering non-traditional income sources, such as self-employment income, rental income, or government assistance programs.

- Income Stability: Conventional loans may place more emphasis on stable, long-term employment. USDA loans, however, may be more lenient in considering borrowers with seasonal or variable income, common in rural areas.

- Residual Income: Conventional loans often require borrowers to have a certain amount of residual income after housing expenses and other debt payments. USDA loans may have lower residual income requirements, ensuring that borrowers have sufficient funds for basic living expenses.

The more flexible income requirements of USDA loans provide a significant advantage for borrowers in rural areas or those with non-traditional income sources. These loans expand access to homeownership for individuals who may not meet the stricter income criteria of conventional loans, promoting economic development and stability in rural communities.

4. Down Payment

The difference in down payment requirements between conventional loans and USDA loans is a critical aspect to consider when exploring home financing options. Conventional loans, offered by private lenders, typically require a down payment, which is a percentage of the home's purchase price paid upfront by the borrower. USDA loans, on the other hand, offer a unique advantage of allowing borrowers to purchase a home with no down payment, making homeownership more accessible to low- and moderate-income families.

The significance of the down payment requirement lies in its impact on the borrower's financial situation and overall affordability of the home. A larger down payment reduces the loan amount needed, resulting in lower monthly mortgage payments and potentially lower interest costs over the life of the loan. However, saving for a substantial down payment can be challenging, especially for first-time homebuyers or those with limited financial resources.

USDA loans address this challenge by eliminating the down payment requirement, making homeownership more attainable for eligible borrowers. This provision is particularly beneficial in rural areas, where incomes may be lower and housing costs may be more affordable. By removing the down payment barrier, USDA loans empower individuals and families to achieve their dream of homeownership, contributing to community development and economic growth in rural regions.

In summary, the contrasting down payment requirements between conventional loans and USDA loans have a significant impact on the accessibility and affordability of homeownership. Conventional loans require a down payment, which can be a hurdle for some borrowers, while USDA loans offer the advantage of no down payment, expanding access to homeownership for low- and moderate-income families, particularly in rural areas.

5. Interest Rates

The difference in interest rates between USDA loans and conventional loans is a significant factor influencing the overall cost of homeownership. Conventional loans, offered by private lenders, typically have higher interest rates compared to USDA loans, which are backed by the US Department of Agriculture. This distinction is rooted in the varying risk profiles associated with each loan type and the government's commitment to promoting affordable housing in rural areas.

Lower interest rates on USDA loans translate into lower monthly mortgage payments, making homeownership more accessible and affordable for low- and moderate-income families. By reducing the cost of borrowing, USDA loans empower individuals and families to achieve their dream of homeownership, contributing to community development and economic growth in rural regions.

The practical significance of understanding the difference in interest rates lies in its impact on the borrower's financial situation. Lower interest rates result in lower monthly payments, freeing up more disposable income for other essential expenses, such as education, healthcare, or retirement savings. Additionally, lower interest rates can reduce the overall cost of the loan over its lifetime, potentially saving borrowers thousands of dollars.

In summary, the lower interest rates offered by USDA loans, compared to conventional loans, play a crucial role in making homeownership more affordable and accessible for low- and moderate-income families in rural areas. Understanding this difference is essential for potential homebuyers to make informed decisions about their financing options and achieve their homeownership goals.

6. Loan Limits

In the context of "conventional vs USDA loans," the difference in loan limits is a crucial factor to consider, particularly for borrowers seeking financing for higher-priced homes. Conventional loans, offered by private lenders, typically have higher loan limits compared to USDA loans, which are backed by the US Department of Agriculture.

- Higher Borrowing Capacity: Conventional loans allow borrowers to access larger loan amounts, providing them with the flexibility to purchase homes in more expensive markets or with desirable features. This expanded borrowing capacity can be advantageous for families or individuals seeking more spacious homes, luxury properties, or homes in high-cost areas.

- Regional Implications: The higher loan limits of conventional loans are particularly relevant in urban and suburban areas, where housing prices tend to be higher. Borrowers in these areas may find conventional loans more suitable for meeting their financing needs.

- Impact on Affordability: While higher loan limits offer greater borrowing capacity, it's important to note that they can also lead to higher monthly mortgage payments and overall borrowing costs. Borrowers should carefully assess their financial situation and long-term affordability before opting for a loan with a higher limit.

- Influence on Housing Market: The availability of conventional loans with higher limits can influence the housing market dynamics in certain areas. By providing access to larger loans, conventional loans can stimulate demand for higher-priced homes, potentially driving up property values and overall market activity.

In summary, the higher loan limits of conventional loans, compared to USDA loans, offer greater borrowing capacity and flexibility, particularly in higher-priced housing markets. However, borrowers should carefully consider the implications on affordability and overall borrowing costs before making a decision that aligns with their financial goals and long-term plans.

7. Property Location

The distinction in property location eligibility between USDA loans and conventional loans is a defining characteristic that shapes the accessibility and availability of home financing options for potential homebuyers. USDA loans, backed by the US Department of Agriculture, are exclusively designed to promote homeownership in rural areas. This geographic restriction is rooted in the program's mission to support economic development and improve the quality of life in underserved communities.

Conventional loans, on the other hand, offered by private lenders, are not subject to such location restrictions. They can be used to finance properties in both urban and rural areas, providing greater flexibility for borrowers seeking homes in various locations.

The practical significance of understanding this property location distinction lies in its impact on housing opportunities and affordability. USDA loans play a vital role in increasing homeownership rates in rural communities, where access to conventional financing may be limited due to lower population density and economic challenges. By targeting these areas, USDA loans address the unique needs of rural residents and contribute to the growth and sustainability of rural regions.

In contrast, conventional loans cater to a broader range of property locations, including urban centers, suburban neighborhoods, and rural areas. This flexibility allows borrowers to explore a wider selection of homes and choose the location that best suits their lifestyle and preferences.

In summary, the differing property location eligibility criteria between USDA loans and conventional loans reflect the distinct objectives of each loan type. USDA loans prioritize rural development, while conventional loans offer greater location flexibility. Understanding this distinction is crucial for homebuyers to make informed decisions about their financing options and identify the loan product that aligns with their property location and homeownership goals.

8. Borrower Eligibility

The distinction in borrower eligibility between USDA loans and conventional loans is a fundamental aspect of understanding "conventional vs USDA loans." USDA loans, backed by the US Department of Agriculture, prioritize making homeownership accessible to low- to moderate-income families and individuals. This focus on underserved populations is a cornerstone of the USDA loan program's mission to promote economic development and revitalize rural communities.

Conventional loans, on the other hand, offered by private lenders, do not have specific income restrictions. They are available to borrowers of all income levels, providing greater flexibility for those seeking home financing. However, conventional loans typically have stricter credit and income requirements compared to USDA loans, making them less accessible to low- and moderate-income borrowers.

Understanding the borrower eligibility criteria for USDA loans and conventional loans is crucial for potential homebuyers to determine which loan product best suits their financial situation and homeownership goals. USDA loans provide a unique opportunity for low- to moderate-income borrowers to achieve homeownership, while conventional loans cater to a broader range of borrowers, including those with higher incomes and stronger credit profiles.

The contrasting borrower eligibility requirements between USDA loans and conventional loans highlight the government's commitment to addressing housing disparities and promoting affordable homeownership for all. USDA loans play a vital role in increasing homeownership rates among low- and moderate-income families, contributing to the economic and social well-being of rural communities.

FAQs on Conventional vs USDA Loans

Understanding the differences between conventional loans and USDA loans is essential for potential homebuyers seeking financing options. Here are answers to some frequently asked questions to clarify common concerns and misconceptions:

Question 1: What are the main differences between conventional and USDA loans?

Conventional loans are offered by private lenders and have stricter credit and income requirements. USDA loans are backed by the US Department of Agriculture and have more flexible credit and income requirements, but are restricted to rural areas and have income limits for borrowers.

Question 2: Which loan type is right for me?

If you have a good credit score, a stable income, and are looking to purchase a home in any location, a conventional loan may be a good option. If you have a lower credit score, a lower income, or are looking to purchase a home in a rural area, a USDA loan may be a better choice.

Question 3: Can I get a USDA loan if I have bad credit?

USDA loans have more flexible credit requirements compared to conventional loans. While having a higher credit score will improve your chances of approval, you may still be eligible for a USDA loan with a lower credit score.

Question 4: Do I need to make a down payment with a USDA loan?

No, USDA loans allow you to purchase a home with no down payment. This can be a significant advantage for low- and moderate-income borrowers who may not have the funds for a large down payment.

Question 5: Are USDA loans available in all areas?

No, USDA loans are only available in eligible rural areas. The USDA website provides a tool to check if a specific property is located in an eligible area.

These FAQs provide a concise overview of the key differences between conventional and USDA loans. By understanding these differences, potential homebuyers can make informed decisions about the financing options that best suit their needs and goals.

Proceed to the next section to explore more detailed information on conventional vs USDA loans.

Conclusion

In summary, conventional loans and USDA loans offer distinct advantages and cater to different borrower profiles. Conventional loans provide greater flexibility in terms of property location and borrower eligibility, but may have stricter credit and income requirements. USDA loans, on the other hand, offer more favorable terms for low- to moderate-income borrowers in rural areas, but come with restrictions on property location and loan limits.

The choice between a conventional loan and a USDA loan depends on the borrower's individual circumstances and financial goals. Understanding the key differences between these loan types is crucial for making an informed decision about the best financing option.

You Might Also Like

The Menzo Case: Witness Accounts And EvidenceDiscover: Time Kills All Deals - A Critical Look At Marketing's Ultimate Truth

Get To Know Kent Masters: The Expert In Real Estate

Uncovering The Wealth Of Carolyn Chambers: An Exploration Of Net Worth

Google Discovery: Uncovering The Insights Of Robert McGraw, Renowned Author

Article Recommendations