Do you know that there are loans for teachers with bad credit?

If you are a teacher with bad credit, you may think that you are not eligible for a loan. However, there are a number of lenders who offer loans specifically for teachers with bad credit. These loans can help you to consolidate your debt, pay for unexpected expenses, or make home improvements.

There are a few things to keep in mind when applying for a loan for teachers with bad credit. First, you will need to find a lender who is willing to work with you. Not all lenders offer loans to borrowers with bad credit, so it is important to do your research. Second, you will need to be prepared to pay a higher interest rate than borrowers with good credit. This is because lenders view borrowers with bad credit as a higher risk. Finally, you will need to make sure that you can afford the monthly payments. If you cannot afford the payments, you could end up defaulting on the loan, which could further damage your credit score.

Despite the challenges, getting a loan for teachers with bad credit can be a great way to improve your financial situation. If you are considering getting a loan, it is important to weigh the pros and cons carefully to make sure that it is the right decision for you.

Loans for Teachers with Bad Credit

Loans for teachers with bad credit can be a valuable resource for educators who need financial assistance. These loans can help teachers consolidate debt, cover unexpected expenses, or make home improvements. However, it is important to be aware of the key aspects of these loans before applying.

- Eligibility: Not all teachers with bad credit will qualify for a loan. Lenders will consider your credit score, income, and debt-to-income ratio when making a decision.

- Interest rates: Loans for teachers with bad credit typically have higher interest rates than loans for teachers with good credit. This is because lenders view borrowers with bad credit as a higher risk.

- Loan terms: The loan terms, such as the loan amount and repayment period, will vary depending on the lender and your individual circumstances.

- Fees: Some lenders may charge fees for loans for teachers with bad credit. These fees can include origination fees, late fees, and prepayment penalties.

- Co-signers: If you have bad credit, you may need to find a co-signer who has good credit to guarantee your loan.

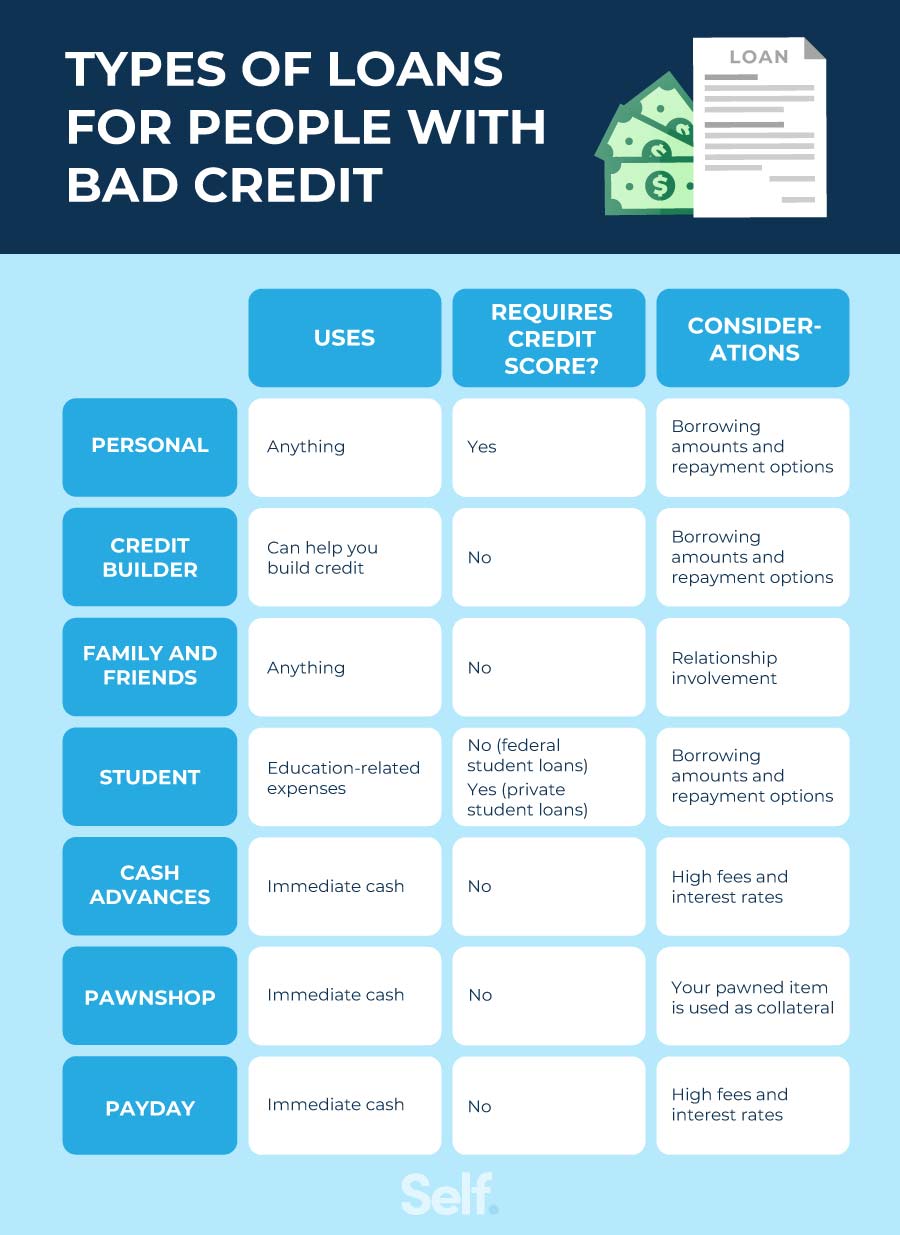

- Alternatives: There are a number of alternatives to loans for teachers with bad credit, such as debt consolidation loans, personal loans, and credit counseling.

- Cautions: Before applying for a loan for teachers with bad credit, it is important to weigh the pros and cons carefully. These loans can be a helpful way to improve your financial situation, but they can also be expensive and difficult to repay if you are not careful.

It is important to note that loans for teachers with bad credit are not a one-size-fits-all solution. The best loan for you will depend on your individual circumstances. It is important to compare the different options available and choose the loan that is right for you.

1. Eligibility

When it comes to loans for teachers with bad credit, eligibility is a key factor. Not all teachers with bad credit will qualify for a loan, as lenders will consider your credit score, income, and debt-to-income ratio when making a decision.

- Credit score: Your credit score is a number that lenders use to assess your creditworthiness. A higher credit score indicates that you are a lower risk to lenders, and you are more likely to qualify for a loan with a lower interest rate. If you have a bad credit score, you may still be able to qualify for a loan for teachers with bad credit, but you may have to pay a higher interest rate.

- Income: Your income is another important factor that lenders will consider when making a decision on your loan application. Lenders want to make sure that you have enough income to repay the loan. If you have a low income, you may not qualify for a loan, or you may only qualify for a small loan amount.

- Debt-to-income ratio: Your debt-to-income ratio is the percentage of your monthly income that goes towards paying off debt. Lenders want to make sure that you have enough income left over to repay the loan after you have paid your other debts. If you have a high debt-to-income ratio, you may not qualify for a loan, or you may only qualify for a small loan amount.

If you are a teacher with bad credit and you are considering applying for a loan, it is important to understand the eligibility requirements. You can improve your chances of qualifying for a loan by improving your credit score, increasing your income, and reducing your debt-to-income ratio.

2. Interest rates

The interest rate on a loan is the cost of borrowing money. It is expressed as a percentage of the loan amount. Interest rates vary depending on a number of factors, including the lender, the loan amount, the loan term, and the borrower's credit score. Borrowers with bad credit are considered to be a higher risk to lenders, so they are typically charged higher interest rates.

The higher interest rates on loans for teachers with bad credit can make it more difficult to repay the loan. This is because a larger portion of the monthly payment will go towards interest, leaving less money to pay down the principal. As a result, it is important to carefully consider the interest rate before applying for a loan for teachers with bad credit.

If you are a teacher with bad credit and you are considering applying for a loan, there are a few things you can do to improve your chances of getting a lower interest rate. These include:

- Improving your credit score

- Increasing your income

- Reducing your debt-to-income ratio

- Finding a co-signer with good credit

3. Loan terms

When it comes to loans for teachers with bad credit, the loan terms will vary depending on a number of factors, including the lender and your individual circumstances. Some of the key loan terms that you should be aware of include:

- Loan amount: The loan amount is the amount of money that you borrow. The loan amount will vary depending on the lender and your individual circumstances, such as your income, debt-to-income ratio, and credit score.

- Repayment period: The repayment period is the length of time that you have to repay the loan. The repayment period will vary depending on the lender and your individual circumstances, such as your income and debt-to-income ratio.

- Interest rate: The interest rate is the cost of borrowing money. The interest rate will vary depending on the lender and your individual circumstances, such as your credit score.

- Fees: Some lenders may charge fees for loans for teachers with bad credit. These fees can include origination fees, late fees, and prepayment penalties.

It is important to understand the loan terms before applying for a loan for teachers with bad credit. You should make sure that you can afford the monthly payments and that you are comfortable with the repayment period. You should also compare the different loan terms offered by different lenders to find the loan that is right for you.

4. Fees

When it comes to loans for teachers with bad credit, it is important to be aware of the potential fees that you may be charged. These fees can include origination fees, late fees, and prepayment penalties.

Origination fees are charged by some lenders to cover the cost of processing your loan application. These fees can range from 1% to 5% of the loan amount.Late fees are charged if you make a payment after the due date. These fees can range from $25 to $50.Prepayment penalties are charged if you pay off your loan early. These fees can range from 1% to 5% of the loan amount.

It is important to factor these fees into your budget when considering a loan for teachers with bad credit. These fees can add to the overall cost of your loan, so it is important to compare the fees charged by different lenders before applying for a loan.

If you are unable to afford the fees associated with a loan for teachers with bad credit, there are a number of other options available to you. These options include:

- Debt consolidation loans: These loans can be used to consolidate your existing debt into a single loan with a lower interest rate.

- Personal loans: These loans can be used for a variety of purposes, including debt consolidation, home improvements, and unexpected expenses.

- Credit counseling: Credit counseling can help you to improve your credit score and manage your debt.

5. Co-signers

When it comes to loans for teachers with bad credit, a co-signer can be a valuable asset. A co-signer is someone who agrees to repay the loan if you are unable to do so. This can give lenders peace of mind and make them more likely to approve your loan application.

- Facet 1: The Role of a Co-signer

A co-signer plays a crucial role in the loan process for individuals with bad credit. They essentially vouch for the borrower's ability to repay the loan, mitigating the lender's risk. Without a co-signer, borrowers with bad credit may struggle to secure loan approval or may only qualify for loans with unfavorable terms and high interest rates. - Facet 2: Finding a Co-signer

Identifying a suitable co-signer can be challenging for borrowers with bad credit. Potential co-signers should have good credit, a stable income, and a willingness to take on the financial responsibility of the loan. Family members, close friends, or colleagues with strong credit profiles are often approached to act as co-signers. - Facet 3: Implications for the Co-signer

Co-signing a loan is not without its risks for the co-signer. If the borrower defaults on the loan, the co-signer becomes legally obligated to repay the debt. This can damage the co-signer's credit score and make it more difficult for them to obtain credit in the future. It's crucial for co-signers to carefully consider their financial situation and the potential implications before agreeing to co-sign a loan. - Facet 4: Alternatives to Co-signers

In some cases, borrowers with bad credit may be able to obtain loans without a co-signer. Some lenders offer loans specifically designed for borrowers with bad credit, albeit often with higher interest rates and stricter eligibility criteria. Additionally, exploring alternative sources of financing, such as government assistance programs or non-profit organizations, can provide options for borrowers who struggle to qualify for traditional loans.

Overall, understanding the role of co-signers in the context of loans for teachers with bad credit is crucial. Co-signers can facilitate loan approval and improve loan terms, but it's essential for both the borrower and co-signer to be aware of the potential risks and implications involved.

6. Alternatives

For individuals with bad credit, obtaining loans can be challenging, and this applies to teachers as well. However, it's important to recognize that loans for teachers with bad credit are not the sole option available. There are several alternatives that can provide financial assistance and support.

Debt consolidation loans combine multiple debts into a single loan with a potentially lower interest rate, making it easier to manage monthly payments and reduce overall debt. Personal loans can also be used to consolidate debt or cover unexpected expenses, offering flexibility and potentially lower interest rates compared to loans specifically designed for bad credit.

Credit counseling is another valuable alternative. Non-profit credit counseling agencies provide guidance and support to individuals struggling with debt. They can help create personalized debt management plans, negotiate with creditors, and provide financial education to improve credit scores over time. Unlike loans, credit counseling focuses on long-term financial well-being and empowers individuals to take control of their finances.

Understanding these alternatives is crucial for teachers with bad credit. By exploring these options, they can find solutions that align with their financial needs and goals. It's important to carefully consider the terms, interest rates, and potential impact on credit scores before making a decision. Seeking professional advice from a credit counselor can provide valuable insights and support in navigating the complexities of financial challenges.

7. Cautions

When considering loans for teachers with bad credit, it is crucial to proceed with caution. While these loans can provide a solution for financial difficulties, there are potential drawbacks and limitations to be aware of. Understanding the caveats associated with these loans is essential for making informed decisions.

- Facet 1: High Interest Rates

Loans for teachers with bad credit often come with higher interest rates compared to loans for individuals with good credit. These higher rates can significantly increase the overall cost of borrowing, making it more challenging to repay the loan in the long run. It is important to carefully evaluate the interest rates and compare them with other loan options before making a decision. - Facet 2: Limited Loan Amounts

Lenders may offer lower loan amounts to borrowers with bad credit due to the perceived higher risk. This can limit the amount of financial assistance available, potentially making it difficult to fully address urgent financial needs or consolidate existing debts. - Facet 3: Strict Eligibility Criteria

Qualifying for loans for teachers with bad credit can be challenging. Lenders often have stricter eligibility criteria, including requirements for minimum income levels, stable employment history, and a manageable debt-to-income ratio. Applicants with severe credit issues may find it difficult to meet these criteria. - Facet 4: Potential Impact on Credit Score

Applying for multiple loans for teachers with bad credit in a short period can result in multiple hard inquiries on your credit report. These inquiries can temporarily lower your credit score, making it even more challenging to qualify for future loans or credit products.

It is important to carefully weigh the potential benefits and drawbacks of loans for teachers with bad credit before applying. Exploring alternative solutions, such as debt consolidation loans, personal loans, or credit counseling, may be more suitable depending on your financial situation and needs. By understanding the cautions associated with these loans and making informed decisions, teachers with bad credit can navigate the lending landscape and improve their financial well-being.

FAQs on Loans for Teachers with Bad Credit

This section addresses frequently asked questions about loans for teachers with bad credit to provide clear and informative answers, helping individuals make informed decisions regarding their financial options.

Question 1: Can teachers with bad credit qualify for loans?

Yes, there are lenders who offer loans specifically designed for teachers with bad credit. However, it is important to note that qualifying for these loans may be more challenging, and the interest rates and loan terms may be less favorable compared to loans for individuals with good credit.

Question 2: What are the eligibility criteria for loans for teachers with bad credit?

Eligibility criteria may vary depending on the lender, but generally, teachers will need to provide proof of employment, income, and a valid teaching license. Lenders will also assess the applicant's credit history and debt-to-income ratio to determine eligibility and loan terms.

Question 3: What interest rates can I expect on a loan for teachers with bad credit?

Interest rates on loans for teachers with bad credit are typically higher than those offered to individuals with good credit. The exact interest rate will depend on factors such as the lender, the loan amount, and the borrower's creditworthiness.

Question 4: What are the repayment terms for loans for teachers with bad credit?

Repayment terms for loans for teachers with bad credit can vary, but typically these loans have shorter repayment periods compared to traditional loans. This means that the monthly payments may be higher, but the loan can be paid off more quickly.

Question 5: Are there any alternatives to loans for teachers with bad credit?

Yes, there are several alternatives to loans for teachers with bad credit. These include debt consolidation loans, personal loans, and credit counseling. It is important to explore all available options and compare loan terms, interest rates, and eligibility criteria to determine the best solution for individual financial needs.

Remember to carefully consider the pros and cons of each option and seek professional advice from a financial expert if needed. By understanding the available options and making informed decisions, teachers with bad credit can find the best financial solution to meet their needs.

Moving forward, we will explore additional strategies for managing finances and improving credit scores for teachers.

Conclusion

In summary, loans for teachers with bad credit offer a potential solution for financial challenges, but it is crucial to proceed with caution and carefully consider the associated drawbacks. These loans often come with higher interest rates, limited loan amounts, and stricter eligibility criteria, making them more expensive and difficult to repay compared to loans for individuals with good credit.

Before applying for a loan for teachers with bad credit, it is essential to weigh the pros and cons, explore alternative solutions, and seek professional advice if needed. Alternative options such as debt consolidation loans, personal loans, and credit counseling may provide more suitable solutions depending on individual financial needs and circumstances.

Furthermore, teachers with bad credit should focus on improving their credit scores over time to access better loan terms and interest rates in the future. This can be achieved by paying bills on time, reducing debt, and building a positive credit history.

By understanding the nuances of loans for teachers with bad credit and exploring all available options, teachers can make informed decisions that align with their financial goals and improve their overall financial well-being.

You Might Also Like

Essential NC Non-Owners Insurance GuideDiscover: Time Kills All Deals - A Critical Look At Marketing's Ultimate Truth

Smart Investing: Buying A Second House And Renting Out Your First For Passive Income

Latest Ciss Stock Forecast And Predictions

The Ultimate Guide To Brian W. Kocher

Article Recommendations