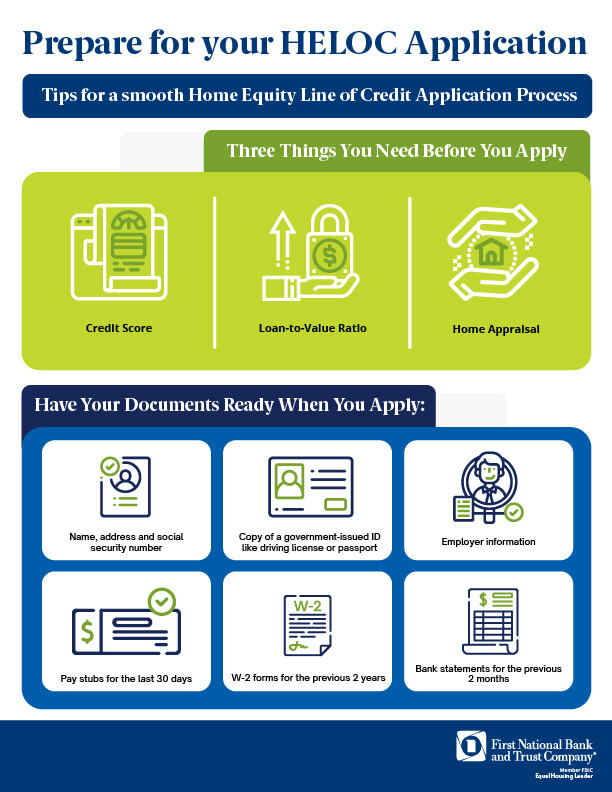

What is HELOC processing time?

HELOC processing time is the amount of time it takes for a lender to process and approve a HELOC application. The processing time can vary depending on the lender, the complexity of the application, and the borrower's financial situation.

Generally, HELOC processing time can take anywhere from a few days to several weeks. However, it is important to note that this is just an estimate, and the actual processing time may vary.

There are a number of factors that can affect HELOC processing time, including:

- The lender's underwriting guidelines

- The borrower's credit history and score

- The borrower's debt-to-income ratio

- The value of the borrower's home

- The amount of the HELOC loan

If a borrower has a strong credit history and a low debt-to-income ratio, they may be able to get a HELOC approved more quickly. However, if a borrower has a lower credit score or a higher debt-to-income ratio, the processing time may be longer.

It is important to factor in HELOC processing time when planning to use a HELOC to finance a project. If a borrower needs the funds quickly, they should choose a lender with a faster processing time.

HELOC Processing Time

HELOC processing time refers to the duration it takes for a lender to review and approve a HELOC application. Several key aspects influence this processing time:

- Application complexity: Complex applications involving multiple properties or income sources may require additional review.

- Credit history: A strong credit history can expedite processing, while a weaker history may lead to delays.

- Debt-to-income ratio: A high debt-to-income ratio can impact processing time as the lender assesses the borrower's repayment capacity.

- Property appraisal: Lenders typically require an appraisal to determine the home's value, which can add to processing time.

- Lender underwriting guidelines: Different lenders have varying underwriting guidelines, affecting processing timelines.

- Loan amount: Larger loan amounts may require more extensive review and documentation.

- Documentation: Incomplete or missing documentation can delay processing.

- Appraisal scheduling: Scheduling and conducting an appraisal can contribute to the overall processing time.

These aspects collectively determine the processing time for a HELOC application. Borrowers can potentially expedite the process by providing complete and accurate documentation, maintaining a strong credit history, and proactively addressing any lender inquiries.

1. Application complexity

The complexity of a HELOC application can significantly impact its processing time. When an application involves multiple properties or income sources, it requires more in-depth analysis and documentation.

- Multiple properties: If the HELOC application includes multiple properties, the lender must evaluate each property's value, condition, and potential risks. This can extend the processing time as the lender gathers and reviews the necessary information.

- Multiple income sources: When a borrower has multiple income sources, the lender must verify and analyze each source to assess the borrower's overall financial stability. This can involve obtaining documentation from employers, banks, or other sources, which can add to the processing time.

In summary, the complexity of a HELOC application, particularly when involving multiple properties or income sources, can lead to additional review and documentation requirements. This can result in a longer processing time compared to simpler applications.

2. Credit history

Credit history plays a crucial role in determining HELOC processing time. A strong credit history, characterized by timely payments, low credit utilization, and a high credit score, can significantly expedite the processing time.

When a borrower has a strong credit history, the lender has greater confidence in their ability to repay the HELOC loan. This reduces the need for additional verification and documentation, streamlining the processing time. Lenders may also offer more favorable terms and interest rates to borrowers with strong credit histories.

Conversely, a weaker credit history, marked by late payments, high credit utilization, or a low credit score, can lead to delays in HELOC processing time. The lender may require more documentation to assess the borrower's financial situation and may need to conduct a more thorough review of the application.

In summary, maintaining a strong credit history is essential for a faster HELOC processing time. Borrowers with weaker credit histories may experience delays and may need to provide additional documentation to support their application.

3. Debt-to-income ratio

The debt-to-income ratio (DTI) is a crucial factor that affects HELOC processing time. DTI measures the borrower's monthly debt obligations relative to their monthly income. A high DTI indicates that a significant portion of the borrower's income is already committed to debt repayment, which can raise concerns about their ability to handle additional debt.

When a borrower has a high DTI, the lender will need to carefully assess their financial situation to determine if they can afford a HELOC. This may involve reviewing additional documentation, such as pay stubs, bank statements, and tax returns. The lender will also want to understand the borrower's plans for using the HELOC funds and how they will fit into their overall budget.

In some cases, a borrower with a high DTI may still be able to qualify for a HELOC, but they may be offered a lower loan amount or a higher interest rate. The lender may also require the borrower to provide additional collateral or a co-signer.

Overall, a high DTI can lead to a longer HELOC processing time as the lender conducts a more thorough review of the borrower's financial situation. Borrowers can improve their chances of getting a HELOC approved quickly by keeping their DTI low.

4. Property appraisal

Property appraisal plays a crucial role in HELOC processing time. Lenders require an appraisal to assess the value of the property that will secure the HELOC loan. This appraisal helps the lender determine the maximum loan amount that can be offered to the borrower.

The appraisal process typically involves a licensed appraiser visiting the property, inspecting its condition, and comparing it to similar properties in the area. The appraiser will then provide a report that estimates the property's value.

Depending on the lender, the appraisal process can take several days or even weeks. This can add to the overall HELOC processing time, particularly if the appraisal uncovers any issues that need to be addressed before the loan can be approved.To expedite the appraisal process, borrowers can ensure that their property is in good condition and that they have all necessary documentation ready, such as proof of ownership and recent utility bills.

5. Lender underwriting guidelines

Lender underwriting guidelines are a crucial component of HELOC processing time. These guidelines establish the criteria that lenders use to assess a borrower's creditworthiness and ability to repay a HELOC loan. Different lenders have varying underwriting guidelines, which can significantly impact the processing timeline.

For instance, some lenders may have stricter guidelines regarding debt-to-income ratios, credit scores, or property values. This means that borrowers who do not meet these stricter criteria may experience delays in the processing of their HELOC application.

Conversely, lenders with more flexible underwriting guidelines may be able to process HELOC applications more quickly. These lenders may be more willing to approve borrowers with lower credit scores, higher debt-to-income ratios, or less valuable properties.

It is important for borrowers to understand the underwriting guidelines of the lender they are applying with. This will help them determine if they are likely to qualify for a HELOC and how long the processing time may take.

Overall, lender underwriting guidelines play a significant role in HELOC processing time. Borrowers can expedite the processing time by choosing a lender with flexible underwriting guidelines that align with their financial profile.

6. Loan amount

The loan amount plays a crucial role in determining HELOC processing time. Larger loan amounts typically require more extensive review and documentation, which can prolong the processing timeline.

- Underwriting and Risk Assessment: Larger loan amounts pose higher risk to lenders, prompting them to conduct more thorough underwriting and risk assessment. This involves scrutinizing the borrower's financial history, income, assets, and debt obligations to gauge their ability to repay the loan.

- Property Appraisal: For HELOCs secured by real estate, larger loan amounts often necessitate a more detailed property appraisal. The appraiser will meticulously inspect the property and analyze market data to determine its accurate value, ensuring that the loan amount is commensurate with the property's worth.

- Loan Documentation: Larger loan amounts require more comprehensive loan documentation, including loan agreements, promissory notes, and other legal documents. These documents must be carefully drafted and reviewed to ensure compliance with regulations and to protect the interests of both the lender and the borrower.

- Legal and Regulatory Compliance: Lenders must adhere to various legal and regulatory requirements when processing larger loan amounts. This may involve additional steps, such as obtaining legal opinions or conducting enhanced due diligence, to ensure compliance with applicable laws and regulations.

In summary, larger loan amounts in HELOC applications trigger more extensive review, documentation, and compliance measures, which can result in a longer processing time. Borrowers seeking larger HELOCs should be prepared for a more rigorous and time-consuming processing experience.

7. Documentation

In the context of HELOC processing time, complete and accurate documentation plays a critical role in expediting the process. Incomplete or missing documentation can lead to delays and potential roadblocks.

- Verification and Underwriting: Financial institutions rely on documentation to verify a borrower's financial history, income, assets, and debt obligations. Incomplete documentation can hinder the verification process, prolonging the underwriting and approval timeline.

- Property Appraisal: For HELOCs secured by real estate, an appraisal is essential to determine the property's value and ensure that the loan amount is commensurate. Missing or incomplete documentation related to the property, such as ownership records or inspection reports, can delay the appraisal process.

- Legal and Regulatory Compliance: Lenders must adhere to strict legal and regulatory requirements when processing HELOCs. Incomplete or missing documentation can hinder compliance efforts, as lenders may need to request additional information or documentation to meet regulatory standards.

- Communication and Coordination: Complete documentation facilitates effective communication between the borrower, lender, and other parties involved in the HELOC process. Missing or incomplete documentation can lead to misunderstandings, delays in communication, and potential setbacks in processing.

In summary, ensuring complete and accurate documentation is crucial for a smooth and timely HELOC processing experience. Borrowers should proactively gather and submit all necessary documentation to avoid delays and potential complications.

8. Appraisal scheduling

Appraisal scheduling plays a significant role in HELOC processing time. An appraisal is a crucial step in the HELOC process, as it determines the value of the property that will secure the loan. The appraisal process typically involves scheduling an appointment with a licensed appraiser, who will visit the property, inspect its condition, and compare it to similar properties in the area.

- Scheduling Availability: Appraisers' schedules can be busy, especially during peak seasons or in high-demand areas. Scheduling an appraisal appointment can take several days or even weeks, depending on the appraiser's availability.

- Property Inspection: The appraiser's inspection of the property can also contribute to processing time. The appraiser will need to carefully examine the property's interior and exterior, which can take several hours, especially for larger or complex properties.

- Comparable Analysis: After inspecting the property, the appraiser will conduct a comparative market analysis to determine its value. This involves researching recent sales of similar properties in the area, which can be a time-consuming process.

- Appraisal Report: Once the appraiser has completed their analysis, they will prepare a written appraisal report. This report typically includes details of the property's condition, comparable sales data, and the appraiser's estimated value of the property.

In summary, the scheduling and conducting of an appraisal can contribute to the overall HELOC processing time. Borrowers should be aware of potential delays and plan accordingly to ensure a smooth and timely HELOC application process.

Frequently Asked Questions about HELOC Processing Time

Understanding HELOC processing time is crucial for borrowers considering a HELOC. Here are answers to some common questions:

Question 1: What is a typical HELOC processing time?

Answer: HELOC processing time can vary depending on several factors, including lender, application complexity, and borrower's financial situation. Generally, it can take anywhere from a few days to several weeks.

Question 2: What factors can affect HELOC processing time?

Answer: Factors include lender's underwriting guidelines, borrower's credit history, debt-to-income ratio, property value, loan amount, and completeness of documentation.

Question 3: How can I reduce HELOC processing time?

Answer: Provide complete and accurate documentation, maintain a strong credit history, reduce debt-to-income ratio, and choose a lender with faster processing times.

Question 4: What should I do if my HELOC application is taking longer than expected?

Answer: Contact the lender to inquire about the status and provide any additional information or documentation they may need.

Question 5: Is it possible to get a HELOC with a fast processing time?

Answer: Yes, some lenders offer expedited processing options, but these may come with additional costs or stricter eligibility criteria.

In summary, HELOC processing time is influenced by various factors, and borrowers can take steps to reduce it. By understanding the process and addressing potential delays, borrowers can navigate the HELOC application process efficiently.

For more information and guidance, consult with a financial advisor or mortgage professional.

HELOC Processing Time

HELOC processing time is a critical aspect to consider when applying for a Home Equity Line of Credit (HELOC). It can vary depending on several factors, including the lender, application complexity, and the borrower's financial situation. Understanding the factors that influence processing time can help borrowers navigate the application process efficiently.

To expedite HELOC processing, borrowers should aim to maintain a strong credit history, reduce their debt-to-income ratio, and provide complete and accurate documentation. They should also consider choosing a lender with faster processing times. By taking these steps, borrowers can increase their chances of obtaining a HELOC with a shorter processing time, allowing them to access the funds they need quickly and conveniently.

You Might Also Like

The Ultimate Guide To Josh Schimmer: Discover His SecretsThe Ultimate Guide To 768x3: Everything You Need To Know

The Definitive Guide To Victor Yu: Learn Everything You Need To Know

Meet Dennis Kogod: Inspiring Leadership And Innovation

Chris Cole's Net Worth: More Than You Think!

Article Recommendations