Are you looking for the best CD rates in Oregon?

A certificate of deposit (CD) is a savings account with a fixed interest rate and a fixed term. When you open a CD, you agree to deposit a certain amount of money for a certain period of time. In return, the bank agrees to pay you a fixed interest rate on your deposit. CD rates vary depending on the bank, the term of the CD, and the amount of money you deposit. However, the best CD rates in Oregon are typically offered by online banks.

There are many benefits to opening a CD. First, CDs offer a higher interest rate than traditional savings accounts. Second, CDs are FDIC-insured, which means that your deposits are protected up to $250,000. Third, CDs can help you save for a specific goal, such as a down payment on a house or a new car.

If you are looking for the best CD rates in Oregon, you should compare rates from multiple banks. You can use a CD rate comparison tool to find the best rates available. Once you have found a good rate, you can open a CD online or at a local bank branch.

Here are some tips for finding the best CD rates in Oregon:

- Compare rates from multiple banks.

- Consider the term of the CD.

- Consider the amount of money you want to deposit.

- Open a CD online or at a local bank branch.

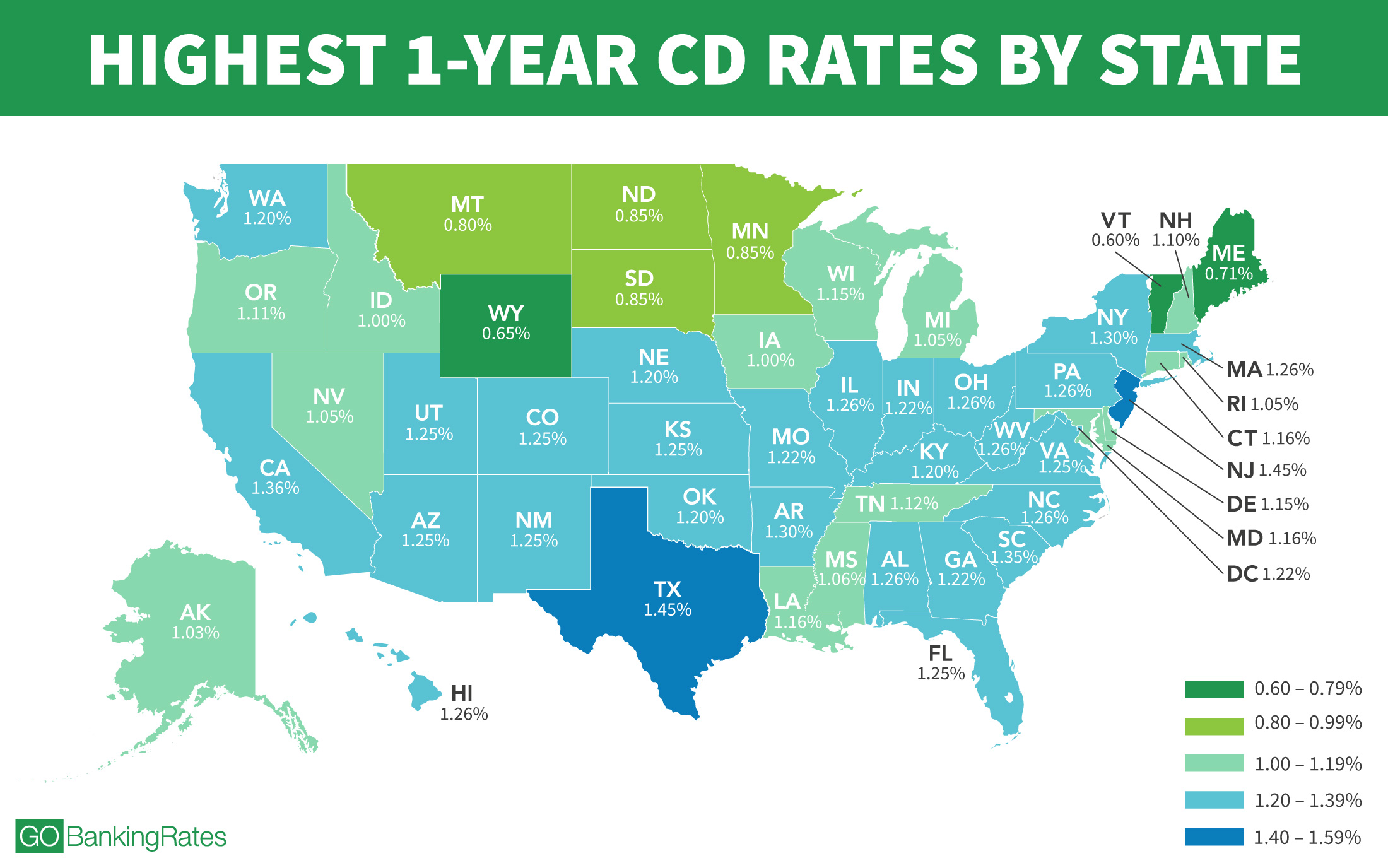

CD Rates Oregon

When it comes to CD rates in Oregon, there are a few key aspects to consider:

- Interest rates: CD rates vary depending on the bank, the term of the CD, and the amount of money you deposit.

- Term length: CD terms can range from a few months to several years.

- Deposit amount: The minimum deposit amount for a CD varies depending on the bank.

- Fees: Some banks charge fees for opening or closing a CD.

- FDIC insurance: CDs are FDIC-insured, which means that your deposits are protected up to $250,000.

- Online vs. traditional banks: Online banks typically offer higher CD rates than traditional banks.

- Compare rates: It's important to compare rates from multiple banks before opening a CD.

By considering these factors, you can find the best CD rates in Oregon and start saving for your future.

1. Interest Rates

Interest rates on certificates of deposit (CDs) in Oregon vary depending on several factors, including the bank, the term of the CD, and the amount of money you deposit. Banks typically offer a range of CD rates, with higher rates for longer terms and larger deposits. It's important to compare rates from multiple banks before opening a CD to ensure you're getting the best possible rate.

- Bank: Different banks offer different CD rates. Some banks may offer higher rates to new customers or customers who maintain a certain balance in their accounts. It's important to shop around and compare rates from multiple banks before opening a CD.

- Term: The term of a CD is the length of time you agree to keep your money in the account. CD terms can range from a few months to several years. Generally, longer terms offer higher interest rates. However, it's important to note that you will not be able to access your money until the CD matures.

- Deposit amount: The amount of money you deposit into a CD can also affect the interest rate you receive. Some banks offer tiered interest rates, which means that you'll earn a higher interest rate on larger deposits.

By understanding how these factors affect CD rates in Oregon, you can make an informed decision about which CD is right for you. It's important to compare rates from multiple banks and choose the CD that offers the best combination of interest rate, term, and deposit amount for your needs.

2. Term length

The term length of a CD is an important factor to consider when choosing a CD, as it affects both the interest rate you will earn and the flexibility you have with your money. In general, longer-term CDs offer higher interest rates than shorter-term CDs. This is because banks are willing to pay a higher rate for your money if they know they will have it for a longer period of time. However, longer-term CDs also mean that you will not be able to access your money until the CD matures. If you need to access your money before the CD matures, you may have to pay a penalty.

When choosing a CD term, it is important to consider your financial goals and risk tolerance. If you are saving for a short-term goal, such as a down payment on a house or a new car, a shorter-term CD may be a good option. If you are saving for a long-term goal, such as retirement, a longer-term CD may be a better option. However, it is important to remember that interest rates can change over time, so it is important to monitor your CD rates and make sure that you are getting the best possible rate.

CD rates in Oregon vary depending on the bank, the term of the CD, and the amount of money you deposit. It is important to compare rates from multiple banks before opening a CD to ensure that you are getting the best possible rate. You can use a CD rate comparison tool to find the best rates available.

3. Deposit amount

The deposit amount is an important factor to consider when choosing a CD, as it can affect both the interest rate you will earn and the flexibility you have with your money. In general, larger deposit amounts will earn higher interest rates. This is because banks are willing to pay a higher rate for your money if they know they will have it for a longer period of time. However, larger deposit amounts also mean that you will have less flexibility with your money. If you need to access your money before the CD matures, you may have to pay a penalty.

When choosing a CD deposit amount, it is important to consider your financial goals and risk tolerance. If you are saving for a short-term goal, such as a down payment on a house or a new car, a smaller deposit amount may be a good option. If you are saving for a long-term goal, such as retirement, a larger deposit amount may be a better option. However, it is important to remember that interest rates can change over time, so it is important to monitor your CD rates and make sure that you are getting the best possible rate.

CD rates in Oregon vary depending on the bank, the term of the CD, and the deposit amount. It is important to compare rates from multiple banks before opening a CD to ensure that you are getting the best possible rate. You can use a CD rate comparison tool to find the best rates available.

4. Fees

When comparing CD rates in Oregon, it is important to consider any fees that may be charged by the bank. Some banks charge a fee for opening a CD, while others charge a fee for closing a CD before the maturity date. These fees can vary depending on the bank and the type of CD. It is important to factor these fees into your decision when choosing a CD, as they can reduce the overall return on your investment.

For example, if you open a CD with a $10,000 deposit and a 5-year term, you may be charged a $25 fee to open the account. If you close the CD before the maturity date, you may be charged a $10 fee. These fees would reduce your overall return on investment by $35. Therefore, it is important to compare CD rates and fees before opening an account to ensure that you are getting the best possible deal.

In addition to opening and closing fees, some banks may also charge other fees, such as maintenance fees or withdrawal fees. It is important to read the terms and conditions of the CD carefully before opening an account to avoid any unexpected fees.

5. FDIC insurance

FDIC insurance is an important factor to consider when choosing a CD, as it protects your deposits up to $250,000. This means that if the bank fails, you will still be able to access your money. FDIC insurance is backed by the full faith and credit of the United States government, so it is a very safe way to save your money.

- What is FDIC insurance?

FDIC insurance is a federal deposit insurance program that protects deposits up to $250,000 at FDIC-member banks. FDIC insurance is backed by the full faith and credit of the United States government, so it is a very safe way to save your money.

- Why is FDIC insurance important?

FDIC insurance is important because it protects your deposits up to $250,000 in the event that the bank fails. This means that you can be confident that your money is safe, even if the bank experiences financial difficulties.

- How does FDIC insurance work?

FDIC insurance works by guaranteeing that depositors will have access to their deposits up to $250,000 in the event that the bank fails. This guarantee is backed by the full faith and credit of the United States government.

- What are the benefits of FDIC insurance?

There are many benefits to FDIC insurance, including:

- Peace of mind knowing that your deposits are safe

- No need to worry about the financial stability of the bank

- Ability to earn a higher interest rate on your deposits

When choosing a CD, it is important to consider the interest rate, term length, and deposit amount. However, it is also important to consider FDIC insurance. FDIC insurance can give you peace of mind knowing that your deposits are safe.

6. Online vs. traditional banks

In the context of "cd rates oregon," it is important to consider the difference between online banks and traditional banks. Online banks typically offer higher CD rates than traditional banks because they have lower overhead costs. This means that they can pass on the savings to their customers in the form of higher interest rates. Additionally, online banks often offer more flexible terms and conditions than traditional banks, making them a more attractive option for consumers.

- Lower overhead costs: Online banks do not have the same overhead costs as traditional banks, such as the cost of maintaining physical branches. This allows them to offer higher CD rates to their customers.

- More flexible terms and conditions: Online banks often offer more flexible terms and conditions than traditional banks, such as the ability to open a CD with a lower minimum deposit or to withdraw money from a CD without paying a penalty. This makes them a more attractive option for consumers who want more flexibility with their savings.

- Higher interest rates: As a result of their lower overhead costs and more flexible terms and conditions, online banks typically offer higher CD rates than traditional banks. This makes them a good option for consumers who want to earn a higher return on their savings.

When choosing a CD, it is important to compare rates from both online banks and traditional banks to find the best deal. However, it is important to remember that the safety of your deposits is the most important factor to consider. Make sure that the bank you choose is FDIC-insured, which means that your deposits are protected up to $250,000.

7. Compare rates

When it comes to "cd rates oregon," it is important to compare rates from multiple banks before opening a CD. This is because CD rates can vary significantly from bank to bank. By comparing rates, you can ensure that you are getting the best possible rate on your CD.

For example, let's say you are looking to open a 1-year CD with a deposit of $10,000. One bank may offer a rate of 1.00%, while another bank may offer a rate of 1.25%. If you were to open a CD with the first bank, you would earn $100 in interest over the course of the year. However, if you were to open a CD with the second bank, you would earn $125 in interest over the course of the year. This is a difference of $25, which is significant.

It is important to note that CD rates can change over time. Therefore, it is important to compare rates from multiple banks on a regular basis to ensure that you are always getting the best possible rate on your CD.

Comparing CD rates is a simple and easy way to save money. By taking the time to compare rates, you can ensure that you are getting the best possible return on your investment.

FAQs about CD rates in Oregon

Here are some frequently asked questions about CD rates in Oregon:

Question 1: What is a CD?

Answer: A certificate of deposit (CD) is a savings account with a fixed interest rate and a fixed term. When you open a CD, you agree to deposit a certain amount of money for a certain period of time. In return, the bank agrees to pay you a fixed interest rate on your deposit.

Question 2: What are the benefits of opening a CD?

Answer: There are many benefits to opening a CD, including:

- Higher interest rates than traditional savings accounts

- FDIC insurance up to $250,000

- Can help you save for a specific goal

Question 3: What are the different types of CDs?

Answer: There are many different types of CDs, including:

- Traditional CDs: These CDs have a fixed interest rate and a fixed term.

- Bump-up CDs: These CDs allow you to increase the interest rate once during the term of the CD.

- Callable CDs: These CDs allow the bank to call back the CD before the maturity date.

Question 4: How do I choose the right CD?

Answer: When choosing a CD, you should consider the following factors:

- Interest rate

- Term length

- Deposit amount

- Fees

- FDIC insurance

Question 5: Where can I find the best CD rates in Oregon?

Answer: You can find the best CD rates in Oregon by comparing rates from multiple banks. You can use a CD rate comparison tool to find the best rates available.

These are just a few of the frequently asked questions about CD rates in Oregon. If you have any other questions, please contact your bank or a financial advisor.

Summary: CD rates in Oregon can vary depending on the bank, the term of the CD, and the amount of money you deposit. It is important to compare rates from multiple banks before opening a CD to ensure that you are getting the best possible rate.

Transition: Now that you know more about CD rates in Oregon, you can start shopping for the best rate. Be sure to compare rates from multiple banks and consider the factors that are important to you, such as the interest rate, term length, and deposit amount.

Conclusion on CD Rates Oregon

In summary, CD rates in Oregon vary depending on the bank, the term of the CD, and the amount of money you deposit. It is important to compare rates from multiple banks before opening a CD to ensure that you are getting the best possible rate. You can use a CD rate comparison tool to find the best rates available.

When choosing a CD, it is important to consider your financial goals and risk tolerance. If you are saving for a short-term goal, such as a down payment on a house or a new car, a shorter-term CD may be a good option. If you are saving for a long-term goal, such as retirement, a longer-term CD may be a better option. However, it is important to remember that interest rates can change over time, so it is important to monitor your CD rates and make sure that you are getting the best possible rate.

CD rates in Oregon are currently competitive, so it is a good time to consider opening a CD if you are looking for a safe and secure way to save your money. By comparing rates and choosing the right CD for your needs, you can earn a higher return on your investment.

You Might Also Like

Discover The Secrets Of 43 63: Your Ultimate GuideJennifer Lee's Net Worth: A Fortune In Animation

Your HELOC: When To Expect Funding After Applying

Get Paid To Promote The Webull Affiliate Program - Earn Big!

Must-Have Replay Sneakers: Elevate Your Footwear Game

Article Recommendations

- Walmart Prescription Delivery

- East Multnomah Soil And Water Conservation District

- Short Positive Quotes About Life Challenges